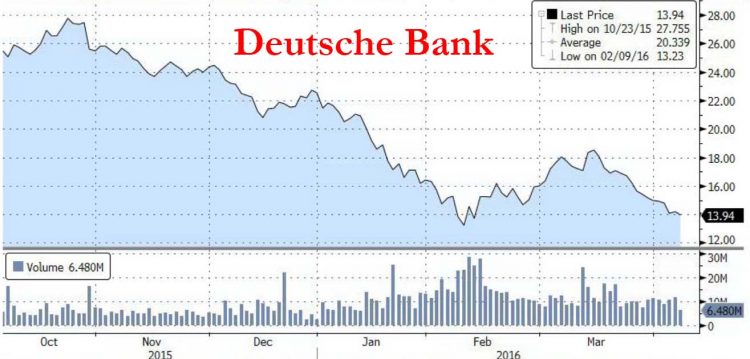

As of this moment, various European banks but most prominently Deutsche Bank…

… as well as Credit Suisse and RBS, have been crashing back to lows hit in early February and then all the way back to the March 2009 “the world is ending” lows.We commented on this yesterday using, ironically enough, a note by Deutsche Bank strategist Jim Reid, in which we showed all the things that were not supposed to happen when Draghi unleashed his massive quad-bazooka QE expansion.

The problem is that now that global central banks are more focused on appeasing China and keeping the USD weaker (by way of a dovish, non-data dependent Fed), the pain for Europe (and Japan), and their currencies, and their banking sector, will likely only get worse. This is precisely the case proposed by Francesco Filia of Fasanara Capital, who explains below his “Short European Bank Thesis.”

Here is his note:

Here below, we update our views on negative rates and our consequential short European Banks equity and sub debt thesis. In a nutshell, we think that not only no bank is ever designed to survive in an environment of deeply negative rates for a prolonged period of time, but their business model is further impaired by negatively sloping interest rate curves. In a twisted unwelcome side-effect following ECB meeting, curves are ever closer to inversion in Europe. They recently became inverted in Japan, for the first time since 1994.

Drivers below, in no particular order:

1. Deeply negative interest rates for a prolonged period of time.

Banks’ business model is at risk. If deeply negative interest rates is the way forward, it doesn’t matter consolidation or bad banks talks or country-specific policymaking (e.g. Italy or Europe): the business model is impaired, needs a rethink/restructuring, even before FinTech is taken into account. No bank is ever designed to function in durable negative rates environment. It is a profitability issue, not a balance sheet problem. Banks’ capitalisation then, however healthy it may seem today, may have to be looked at as no more but the number of years of negative profitability it can withstand before a recap is eventually needed. A fragile banking sector is the Achilles heel of the equity market overall, paving the way for gap risks to the downside.