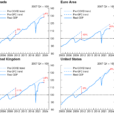

June Inflation Misses Expectations

Last week’s CPI miss has seen some repricing of BOE rate-hike expectations as the market dials back its hawkish view. UK Inflation had been forecast to print 2.7% in June, but printed 2.6%, falling back from 2.9% prior. Pricing for the August meeting reached a peak of around 30% in late June and has now fallen to around 10%. Indeed, repricing for year-end has been even more dramatic falling from around 75% at the end of June to around 45% currently. Clarity on the BOE’s views, given at their recent meeting, along with the inflation miss has seen investors pairing back their hawkish forecasts especially as the majority of the MPC argued that August is too early for a hike.

Hawks’ Main Points in Question

The main argument put forward by MPC hawks has been focused on two elements:

1) The pass through from the decline in the Sterling exchange rate would be deeper and more sustained than expected;

2) Based on strong business investment, the economy would rebalance away from weakness in consumption.

The consequences of a rebalancing in the economy appear tempered so far. The resilience shown in the recent Retail Sales print highlight a strong recovery following weakness in Q1. With wages stable and unemployment at lows, the main channel through which consumption could fall further is a decline in real incomes. However, there is currently little sign of rebalancing fuelled by business investment as leading indicators remain modest. As such, the Hawks’ main arguments appear offside as consumption growth is constrained and a rebalancing of the economy is yet to take hold.

UK Inflation Remains Key

Despite the weak point in June, the risks for inflation remain skewed to the upside going forward through June’s miss will certainly take some hawkish pressure off the BOE in the near term. The sample of inputs for the BOE’s August Inflation Report is now almost complete (around 80%).Comparing the inputs so far against those collected at the time of the May Inflation Report, Oil has fallen around 12% in GBP terms with Gas prices have also fallen, though the 2.5% decline in trade-weighted GBP partially mitigates this. The market path for rates is also far more hawkish than the May report, and the BOE is likely to revise its targets up for 2017 and potentially push the peak inflation level further out to Q1 2018.