Wesco Aircraft (WAIR) sparked my interest after ranking value attributes for a basket of over 3,000 companies. At first, it was the large debt reduction since 2014. Then the aggressive and historical outsized insider buying over the past two months, mean reverting stock performance with a -44% 52-week price change near 52 week low. Enterprise value decline of 50% from the first fiscal quarter ending March 2014 (3,190.560M) to 08/24/17 (1,605.856M). Further, a renewed interest by patient value institutions reporting additional buying for the quarter reported 06/30/17. These and other attributes warranted a closer examination into Wesco Aircraft Holdings.

Wesco Aircraft is one of the largest international distributor and provider of supply chain management services to the aerospace industry. The company offers aerospace products, including hardware, chemical, and electrical with over 565,000 active SKU. Founded in 1953 with 50 locations and 1.50Billion in 2016 sales. The Company’s Services include Quality Assurance, Kitting, and JIT Supply Chain Management.Industries served are commercial aerospace, aviation, defense, energy, pharmaceutical, and electronics.

It’s been several years of an endless string of self-made failures that destroyed large amounts of shareholder value.

The Carlyle Group acquired Wesco back in 2006 and took it public in 2011. Since the IPO it’s been a slow steady market and intrinsic value destroying decline. Recent goodwill write-offs are from poor acquisition. This helped drive selling. Wesco purchased Interfast during 2012 for CDN$134 million cash. Interfast offers fastener-based solutions for a wide range of applications globally. Then, Haas group bought in 2014 for 550M cash. The Haas Group reported 573.5 million in 2012 revenues as a global provider of chemical supply chain management solutions to the commercial aerospace, airline, military, energy, and other markets. Additionally, margins dropped from the low 20% to current high single digits.

During Q3 2017 earning call management presented slides to explain the current issues and go forward plan. But, analysts on the call were tired of excuses. Scathing comments such as “Haas (acquisition) has been a disaster”, “has the board hired a banker and is reviewing the present value of what one can achieve today – or the value achieved today versus the present value of your operating plan that you’re developing”. Additional comment made, “how spectacular this thing went off the rails from when the company first went public, it’s remarkable.”

Management’s responded to analysts concerns with the following comments. The “entire board is committed to doing what’s best for the shareholders, and that includes evaluating any alternative strategies to maximize that long-term shareholder value”. “No. We have not hired a banker yet. And again, my focus is on turning this thing around.” “Our job right now and our focus and our priority is to turn this around”. “I know that the entire board is committed to doing what’s best for the shareholders, and that includes evaluating any alternative strategies to maximize that long-term shareholder value.” “It’s fixable. As I said at the beginning and a couple of times through my prepared remarks, a lot of this is self-inflicted.”

Tangible measures* listed below may hint WAIR is near a market bottom.

Below are favorable summary attributes* with supporting tables.

*Tangible net assets grew from 03/2014 negative -104.230M to the MRQ balance of positive 239.121M or an increase of 343.351M. The main driver of this improvement is the 395.592M debt reduction. In contrast, total equity dropped during the same 2014 to MRQ period from 992.290M to 687.810M or a decline of 304.480M. This in comparison to a net tangible increase of 343.351M. The main driver for the equity decline is the intangible/goodwill write-off of 647.831M

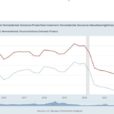

*Market over reaction to the downside with a 50% drop in enterprise value from the first fiscal quarter ending March 2014 (3,190.560M) to 08/24/17 (1,605.856M). A mean reverting -44% 52-week price change. Now trades near its 52 week low of $6.95 off 52 week high of $15.77.