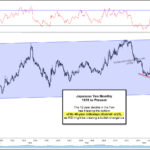

Everyone wants to talk about rates these days and it’s no mystery why.

The Fed is under new leadership at a pivotal juncture. Balance sheet rundown has commenced and the Trump administration has embarked on what multiple sellside desks (see here, here, and here for a few takes) have described as an ill-advised quest to try and supercharge an already hot economy with late-cycle expansionary fiscal policy.

And so, the supply/demand dynamic in the Treasury market has shifted. Financing the tax cuts and increased spending means more supply and with the Fed out of the market, it’s left to price sensitive private investors to provide the bid. This comes as the global reserve diversification debate heats up and as second-order effects of increased bill supply could further sap foreign demand for U.S. debt (see here). To be sure, the market will clear – the question is, at what price?

That gets to the heart of the debate about where yields go from here and the concern is that between everything said above and the suspicion that between fiscal stimulus and now tariffs, price pressures could build quickly, the Fed will be forced to take a hawkish turn that’s not yet priced in by markets. All of these concerns helped fuel the bond rout that conspired with the February 5 vol. shock to send global equities careening into correction territory last month.

Well, one person you might be interested in hearing from on all of this is Jim Grant, and happily, Erik Townsend welcomed him to the MacroVoices podcast this week.

You can listen to the interview in full below, but here are a couple of excerpts that touch on the questions everyone wants answered.

On Jerome Powell:

Erik: What is your expectation? Is Jay Powell a good pick to replace Janet Yellen? Do you think that we’re going to see a change in policy from the Powell Fed as opposed to the Yellen Fed? And what’s your overall reaction to the state of the Fed, so to speak?

Jim: Well, Jay Powell has one commanding credential. And that credential is the absence of a PhD in economics on his resume. I say this because we have been under the thumb of the Doctors of Economics who have been conducting a policy of academic improv. They have set rates according to models which have been all too fallible. They lack of historical knowledge and, indeed, they lack the humility that comes from having been in markets and having been knocked around by Mr. Market (who you know is a very tough hombre).

Jay Powell at least has worked in private equity. He knows a little bit about the business of buying low and selling high. Also he’s a native English speaker. If you listen to him, he speaks in everyday colloquial American English, unlike some of his predecessors. So I’m hopeful. But not so hopeful as to expect a radical departure from the policies we have seen.