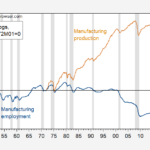

Back in March, the Kansas City branch of the Federal Reserve stated the obvious. US home construction was stuck near the lowest level in the 60 years of records being kept. Despite a decade having passed since the prior bust turned to boom, and with the economy booming, it was apparently worth mentioning.

Obviously, it wasn’t obvious to everyone since the published report was picked up across the US media incredulous to its findings. The Wall Street Journal went so far as to call it this country’s next housing crisis.

America is facing a new housing crisis. A decade after an epic construction binge, fewer homes are being built per household than at almost any time in U.S. history.

That’s the thing about economic depression. In recession, it passes and barely anyone notices once it’s gone. The dot-com instance was so mild, for example, most still associate it with September 11 though it began months beforehand.

Experiencing a prolonged macro event tends to change peoples’ behaviors for them. The generation that made the twenties roar is the same one that became so fiscally frugal to the point of extremes after the thirties. With very good reason. Some people are forced to appreciate these extremes.

Among the most prominent of those is liquidity risk. This works both ways. For businesses, they become reluctant to take on new liabilities (this labor shortage companies don’t seem too willing to do much about). For consumers, they aren’t so cavalier about life altering decisions as they once were.

In terms of housing, these are pretty simple. Where flipping homes fifteen years ago had become a fun game of who can oversize the most, over the last ten years people now prize financial stability. That starts with their view of the labor market, which may, in fact, be very different from how it is described every day in the Wall Street Journal (and its near constant anecdotes in lieu of actual data about this labor shortage).