Image Source: Pixabay

Image Source: Pixabay

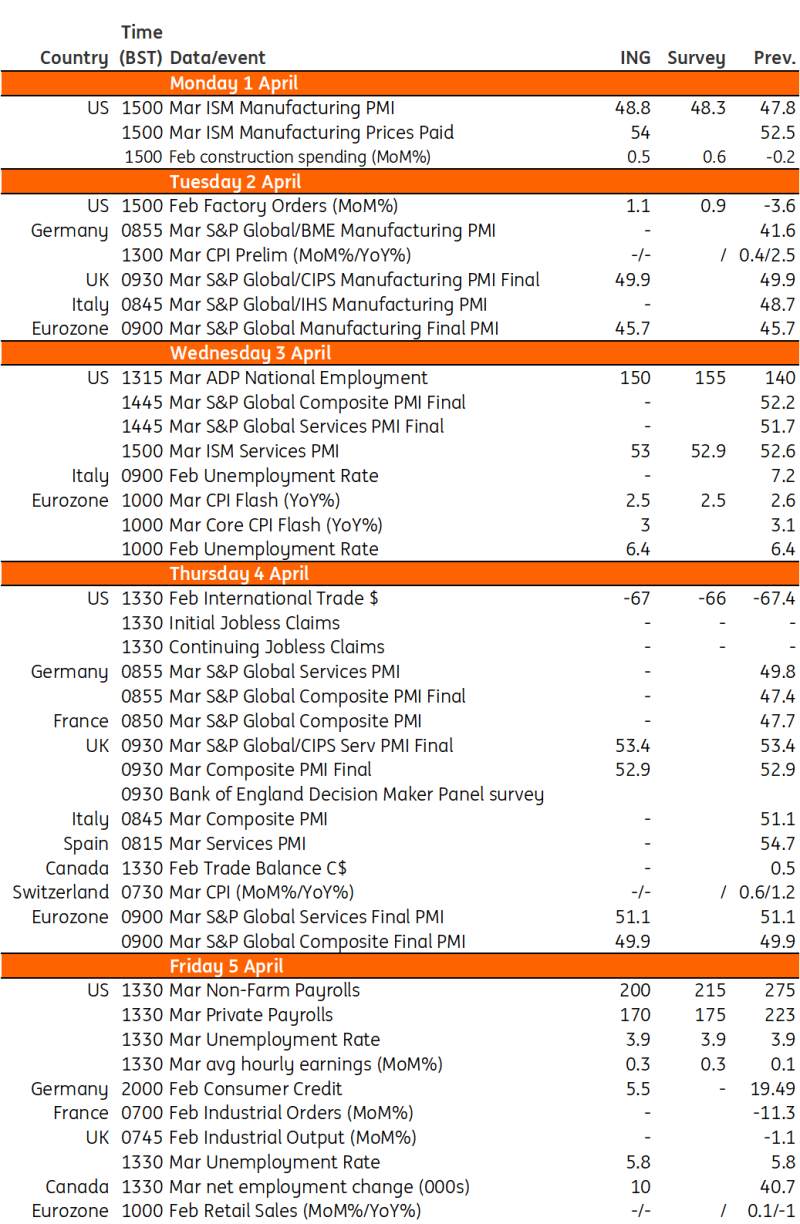

Inflation and labor market data will be in the spotlight in the Eurozone next week. We expect services inflation to be impacted by the Easter effect and unemployment to remain unchanged. The US jobs report will also be in focus, with payrolls expected to rise by just under 200k. In the UK, the BoE’s CFO survey will likely show further inflation progress.

US: Payrolls expected to rise by just under 200KThe jobs report will be the main focus in the US next week. Payrolls are expected to rise by just under 200k, but once again are likely to be concentrated in just three sectors – local government, leisure and hospitality, and private education and healthcare services. 80% of all the jobs added over the past 14 months have come from these sectors and we don’t see much change given that employment surveys have pointed to a slowdown in hiring. The unemployment rate is expected to remain at 3.9% with wage growth remaining benign. We suspect this will keep market pricing for a June federal reserve interest cut at around 80%. Expectations will be firmed up ahead of time with ADP payrolls and the ISM surveys released before next Friday’s jobs figures.

Eurozone: Services inflation expected to come in higher in MarchNext week’s Eurozone data will focus on both inflation and the labor market. Inflation had been high month-on-month in February and January thanks to various reasons related to government measures and stronger than hoped for services inflation. In March, services inflation will be impacted by the Easter effect again, as the holiday comes early this year. That adds to inflation due to early holidays but should subtract from it in May. For the European Central Bank, it will not be easy to look through all of this ahead of the April governing council meeting –but as ECB President Christine Lagarde stated at the March press conference, we’ll know a lot more in June.

UK: Bank of England CFO survey to show further inflation progressThe Bank of England has said it is watching services inflation and wage growth to guide policy this year, but we also know it pays close attention to its in-house survey of Chief Financial Officers. This has been pointing to less aggressive expectations of price rises among companies, but wage growth expectations have been stuck at around 5% for some time. Those expectations did tick lower in the February survey though, and we’ll be looking to see if pay growth is scaled back further in the next survey due next week.This survey won’t move the dial for the BoE’s May meeting, where we still think a rate cut is unlikely. But if we get more progress on this survey measure, coupled with some favorable data on CPI for April/May, this could bring a June cut into play. For now, we’re sticking with our call for an August rate cut – but it’s a relatively close call.

Key events in developed markets next week Image Source: Refinitiv, INGMore By This Author:Japan: Stronger-Than-Expected Retail Sales, Softer-Than-Expected Industrial Production Korea: Industrial Production Rebounded While Construction And Retail Sales Weakened In FebruaryAsia Week Ahead: RBI On Hold, Rising Regional Inflation And A Potential China PMI Data Rebound

Image Source: Refinitiv, INGMore By This Author:Japan: Stronger-Than-Expected Retail Sales, Softer-Than-Expected Industrial Production Korea: Industrial Production Rebounded While Construction And Retail Sales Weakened In FebruaryAsia Week Ahead: RBI On Hold, Rising Regional Inflation And A Potential China PMI Data Rebound