Image Source: PixabayDespite exceeding their quarterly top and bottom line expectations on Thursday, Nike (NKE – Free Report) and Lululemon (LULU – Free Report) shares fell in today’s trading session due to softer-than-expected guidance.Still, investors may be wondering if it’s time to buy the dip in these prominent retailers with Nike’s stock now down -13% year to date while Lululemon shares have fallen -20%.

Image Source: PixabayDespite exceeding their quarterly top and bottom line expectations on Thursday, Nike (NKE – Free Report) and Lululemon (LULU – Free Report) shares fell in today’s trading session due to softer-than-expected guidance.Still, investors may be wondering if it’s time to buy the dip in these prominent retailers with Nike’s stock now down -13% year to date while Lululemon shares have fallen -20%. Image Source: Zacks Investment ResearchFavorable Quarterly ResultsReporting its fiscal third quarter results yesterday, Nike posted earnings of $0.98 per share which climbed 24% year over year and crushed Q3 expectations of $0.69 a share by 42%. Quarterly sales of $12.42 billion were slightly up from $12.39 billion a year ago and beat estimates by 1%. Notably, Nike has exceeded earnings expectations in three of its last four quarterly reports posting an average earnings surprise of 22.55%.

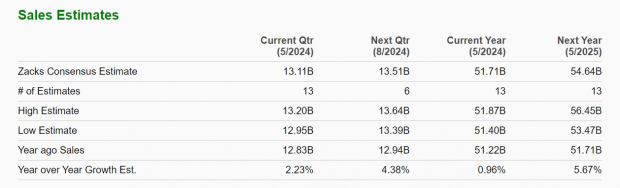

Image Source: Zacks Investment ResearchFavorable Quarterly ResultsReporting its fiscal third quarter results yesterday, Nike posted earnings of $0.98 per share which climbed 24% year over year and crushed Q3 expectations of $0.69 a share by 42%. Quarterly sales of $12.42 billion were slightly up from $12.39 billion a year ago and beat estimates by 1%. Notably, Nike has exceeded earnings expectations in three of its last four quarterly reports posting an average earnings surprise of 22.55%. Image Source: Zacks Investment ResearchTurning to Lululemon, it reported Q4 earnings of $5.29 per share which beat estimates by 5% and soared 20% from $4.40 a share in the comparative quarter. Fourth quarter sales leaped 15% to $3.2 billion and came in slightly above estimates of $3.18 billion. More impressive, Lululemon has now surpassed earnings expectations for 15 consecutive quarters posting an average earnings surprise of 9.68% in its last four quarterly reports.

Image Source: Zacks Investment ResearchTurning to Lululemon, it reported Q4 earnings of $5.29 per share which beat estimates by 5% and soared 20% from $4.40 a share in the comparative quarter. Fourth quarter sales leaped 15% to $3.2 billion and came in slightly above estimates of $3.18 billion. More impressive, Lululemon has now surpassed earnings expectations for 15 consecutive quarters posting an average earnings surprise of 9.68% in its last four quarterly reports. Image Source: Zacks Investment ResearchWeaker Sales GuidanceThe fret of Nike and Lululemon losing their mojo comes as both apparel titans gave softer revenue guidance. Nike still expects its total sales to be up 1% in fiscal 2024 which is roughly on par with Zacks estimates. However, the iconic gym shoe designer warned of a single-digit decline in revenue during the first half of FY25 as it works on innovating its product portfolio in what it called a subdued economic environment.

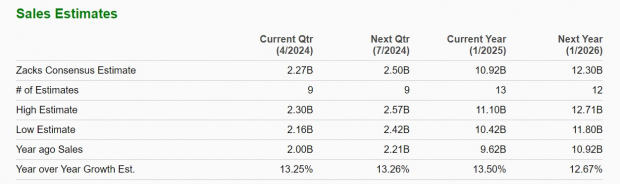

Image Source: Zacks Investment ResearchWeaker Sales GuidanceThe fret of Nike and Lululemon losing their mojo comes as both apparel titans gave softer revenue guidance. Nike still expects its total sales to be up 1% in fiscal 2024 which is roughly on par with Zacks estimates. However, the iconic gym shoe designer warned of a single-digit decline in revenue during the first half of FY25 as it works on innovating its product portfolio in what it called a subdued economic environment. Image Source: Zacks Investment ResearchMeanwhile, Lululemon attributed softer-than-expected sales guidance for its upcoming fiscal first quarter to slower consumer demand. The yoga-inspired apparel company expects Q1 sales of $2.17 billion to $2.2 billion with Zacks estimates at $2.27 billion (Current Qtr). Additionally, Lululemon forecasts total sales for its current FY25 to be in the range of $10.7-$10.8 billion which would be an 11-12% increase with Zacks estimates at $10.92 billion or 13% growth.

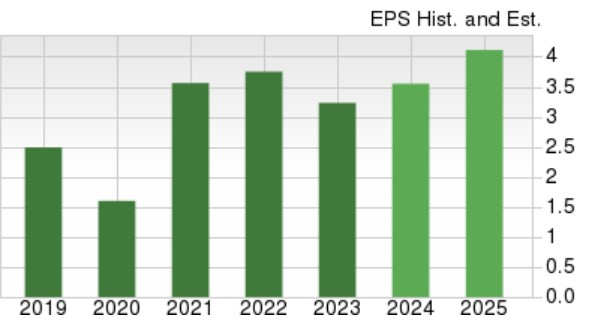

Image Source: Zacks Investment ResearchMeanwhile, Lululemon attributed softer-than-expected sales guidance for its upcoming fiscal first quarter to slower consumer demand. The yoga-inspired apparel company expects Q1 sales of $2.17 billion to $2.2 billion with Zacks estimates at $2.27 billion (Current Qtr). Additionally, Lululemon forecasts total sales for its current FY25 to be in the range of $10.7-$10.8 billion which would be an 11-12% increase with Zacks estimates at $10.92 billion or 13% growth. Image Source: Zacks Investment ResearchEarnings OutlookNike left its full-year net income expectations for FY24 unchanged with its EPS projected to rise 9% to $3.54 per share based on Zacks estimates. Fiscal 2025 earnings are currently forecasted to jump another 16% to $4.12 per share.

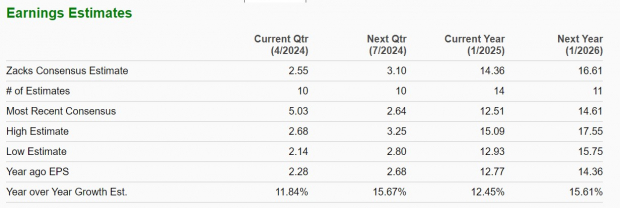

Image Source: Zacks Investment ResearchEarnings OutlookNike left its full-year net income expectations for FY24 unchanged with its EPS projected to rise 9% to $3.54 per share based on Zacks estimates. Fiscal 2025 earnings are currently forecasted to jump another 16% to $4.12 per share. Image Source: Zacks Investment ResearchPivoting to Lululemon, it offered EPS guidance for Q1 in the range of $2.35-$2.40 with Zacks estimates calling for earnings of $2.55 per share or 12% growth. Lululemon expects its full-year EPS for FY25 to be between $14.00-$14.20 which was below the current Zacks Consensus of $14.36 per share and over 12% growth. Furthermore, FY26 EPS is expected to expand another 15% to $16.61 per share based on Zacks estimates.

Image Source: Zacks Investment ResearchPivoting to Lululemon, it offered EPS guidance for Q1 in the range of $2.35-$2.40 with Zacks estimates calling for earnings of $2.55 per share or 12% growth. Lululemon expects its full-year EPS for FY25 to be between $14.00-$14.20 which was below the current Zacks Consensus of $14.36 per share and over 12% growth. Furthermore, FY26 EPS is expected to expand another 15% to $16.61 per share based on Zacks estimates. Image Source: Zacks Investment ResearchBottom LineWhile Nike and Lululemon do appear to be struggling with their growth expectations both stocks currently land a Zacks Rank #3 (Hold). With that being said, longer-term investors could be rewarded for holding stock in these consumer-centric giants at their current levels although short-term economic headwinds could alter their growth trajectories. More By This Author:5 Reasons to Buy Housing ETFs Now3 Invesco Mutual Funds To Build A Solid Portfolio Bull Of The Day: General Motors

Image Source: Zacks Investment ResearchBottom LineWhile Nike and Lululemon do appear to be struggling with their growth expectations both stocks currently land a Zacks Rank #3 (Hold). With that being said, longer-term investors could be rewarded for holding stock in these consumer-centric giants at their current levels although short-term economic headwinds could alter their growth trajectories. More By This Author:5 Reasons to Buy Housing ETFs Now3 Invesco Mutual Funds To Build A Solid Portfolio Bull Of The Day: General Motors