TM Editors’ note: This article discusses a penny stock and/or microcap. Such stocks are easily manipulated; do your own careful due diligence. Image Source: Pixabay

Image Source: Pixabay

Intelligent Bio Solutions (Nasdaq: INBS) is a medical technology company developing and commercializing innovative, intelligent, rapid, noninvasive testing solutions. They are now catching their stride with commercializing their first razor-razorblade product solution, which is an intelligent fingerprinting machine that is supplanting the traditional methods of drug testing. These typically include saliva and urine tests which are biohazardous, time-consuming, and more expensive methods of workplace drug testing. Intelligent Bio Solutions is primed to take significant market share in this industry which is expected to grow from $5.8 billion in 2023 to $28.3 billion in 2032, with workplace testing and urine testing accounting for the largest segments in the group. We believe Intelligent Bio Solutions is growing quickly and is on a short path to profitability, so INBS shares appear significantly undervalued. In this article, Intelligent Bio Solutions’ technology, growth, and potential valuation will be examined—the company should be a multi-bagger if it continues along its current path of rapid growth.

Background on Intelligent Bio Solutions

Intelligent Bio Solutions used to be called GBS, Inc., a company focused on developing biosensors for diabetes management, until it acquired Intelligent Fingerprinting in October 2022, which allowed it to focus its operations on a commercially-ready product. Intelligent Fingerprinting’s product fit in with GBS’s focus, and now the fairly newly-formed entity will be able to grow its profits, supporting the further development of the company’s legacy development project, the biosensor, a protein-transistor hybrid technology designed to sense saliva glucose levels and output an electrical signal based on that. The intelligent fingerprinting drug screening platform is a separate technology that makes use of drug and drug metabolites in fingerprint sweat to inform drug use, which companies can use for drug screening such as fit-for-duty determinations. This platform is growing very rapidly in the global marketplace and will serve as a foothold for the company to grow its global sales, additional potential strategic acquisitions, and further development of the biosensor.INBS shares have been beaten down as most small, unprofitable medtech and biotech companies have been beaten down in the last 2-3 years since the COVID healthcare market bubble. While other unprofitable companies (particularly early-stage biotech companies with no revenue in line-of-sight) have continued to struggle to stay afloat, Intelligent Bio Solutions has arguably reached a turning point in its financial strength as it recently completed an above-market financing and is approaching cash-flow positive operations from which it will be able to either grow more aggressively, acquire new technologies, or further develop its biosensor.

Recent Events

Investors recently exercised warrants at $2.923/share for a total of $1.77 million while shares were trading slightly below this value, in exchange for receiving the same number of warrants at $4.50 per share. This is a favorable transaction considering many financing deals may include shares and warrants where investors sell the shares and keep the warrants, which puts additional pressure on a stock’s market price. This financing was followed by an at-the-market equity raise for $10.1 million at $4.55/share, which included shares and warrants exercisable at the same price. The recent financings de-risks the investment thesis for existing and prospective investors.The company’s shares have traded below the recent financing price even though they posted robust growth of 114% YoY growth for the fiscal second quarter and 337% YoY for the six months ending December 31, 2023. As such, the company is currently valued at around 3x annualized sales despite growing at such a rapid pace and pushing through its infancy as a commercial company. The company is set to continue growing at a rapid pace because its management team is seasoned in medtech and logistics, and the company has a highly valuable and differentiated product that should continue to disrupt the drug screening marketplace, all backed up by a recently-padded balance sheet. The company has a tiny market cap which is not reflective of their recent commercial success.

Intelligent Fingerprinting

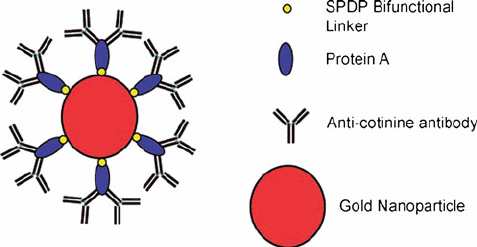

BackgroundThe Intelligent Fingerprinting Drug Screening System evolved from professor David Russell’s early research at the University of East Anglia in Norwich, England, where he worked on detecting drug metabolites in fingerprint sweat using gold nanoparticle-flourescent antibody conjugates, (or antibody tethered magnetic particles) which were designed with various antibodies to detect chemicals such as: cotinine (a metabolite of nicotine) from tobacco users, benzoylecgonine (a metabolite of cocaine) from cocaine users, morphine (a metabolite of heroin) from heroin users, and methadone and its metabolite (EDDP) from patients undergoing drug dependency treatment. It was also shown that dual drug use could be detected; two different drug metabolites were detected in a single fingerprint from individuals using both cocaine and heroin.

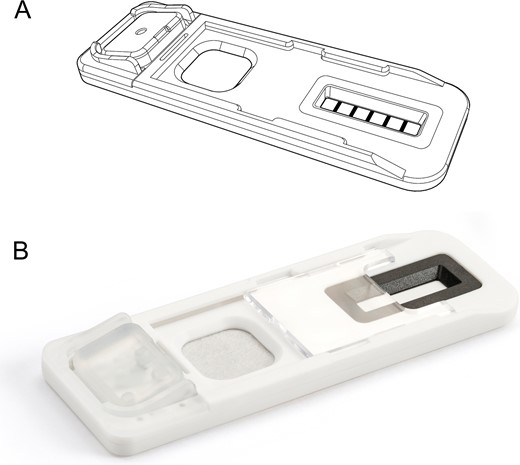

This earlier research eventually gave rise to what is currently being marketed by Intelligent Bio Solutions, the Intelligent Fingerprinting Drug Screening System which uses a similar concept of fluorescent antibody-based drug binding. The Intelligent Fingerprinting Drug Screening System consists of Drug Screening Cartridges and the DSR-plus Reader. The DSR-plus Reader is the “razor” in the razor-razorblade model and it reads drug test results from the fingerprint sweat-bearing Drug Screening Cartridge, the “razorblade,” to determine a positive or negative readout for each drug (or metabolite) in a set of drugs.

How It WorksThe way the portable reader sees drugs in fingerprint sweat is by detecting a set of fluorescence lines (or lack thereof) from a tamper-evident Drug Screening Cartridge. The subject impresses their fingering in a spot on the cartridge which collects the subject’s fingerprint sweat.

A button on the cartridge is then depressed to introduce buffer solution to the print area. The cartridge uses lateral flow of the subject’s sweat, as well as the cartridge’s buffer solution which contains fluorescence-labeled antibodies, across drug-protein conjugate lines (see picture below) present in the drug screening cartridge’s print area to detect the specific drugs or their metabolites.

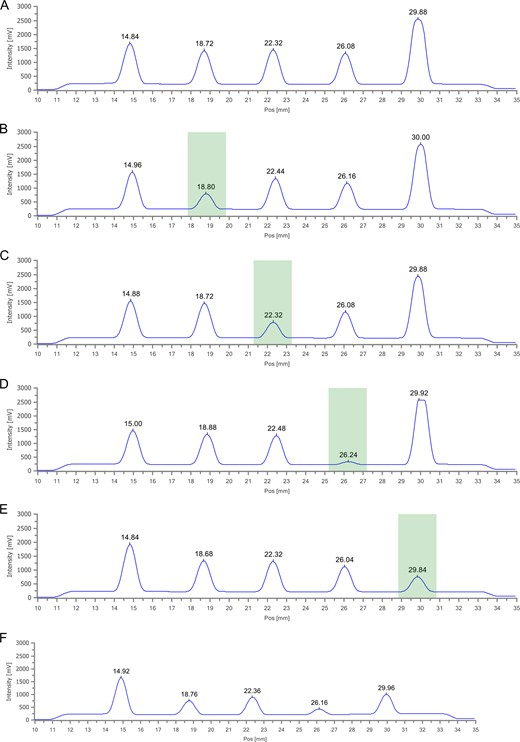

Drug present in fingerprint sweat causes competitive inhibition of the antibodies so that they don’t bind as much to the drug-BSA conjugate lines. In this way, less fluorescence on the drug-protein conjugate line indicates more antibody binding within the sweat (and not on the drug lines) and a positive test result. An example of a fluorescence reading can be found below. The first row is a control, where every fluorescence peak is high, while the 2nd-5th (green bars) show each specific drug, while the 6th row is all 4 drugs (in this one, all four drug lines (2nd-5th peaks) are lower). A range of light spectrum is measured inside of the DSR-plus Reader as it uses an infrared camera and a photo.

Fluorescence intensity profiles for the four drug panel lateral flow assay: Peaks due to the control (HAM), THC, BZE, MOR and AMP are at 14.8, 18.7, 22.3, 26 and 29.8 mm, respectively. (A) No spike, just buffer only, (B) 240 pg THC spike, (C) 90 pg BZE spike, (D) 70 pg MOR spike, (E) 190 pg AMP spike and (F) A combined spike showing signal decrease of all four peaks associated with the four drugs.

DSR reading method: flourescence intensity profiles

Accuracy

The Intelligent Fingerprinting Cartridge is inserted into the portable DSR-Plus, which is a highly sensitive fluorescence measurement instrument that returns a positive or negative result for each drug in the test within minutes. Early accuracy results showed promise and as the screening system was further tested, results improved. Current specificity and sensitivity are in high 90%; however, with any drug test, there are always disputes. In these cases, a sample collection up for dispute is sent to a third party lab, where there has been methods approved by independent bodies to confirm a positive test. The system can be used to test for most drugs—any four drug combination for one system/fingerprint cartridge, but the company sells their standard package to 95% of their customers so far.

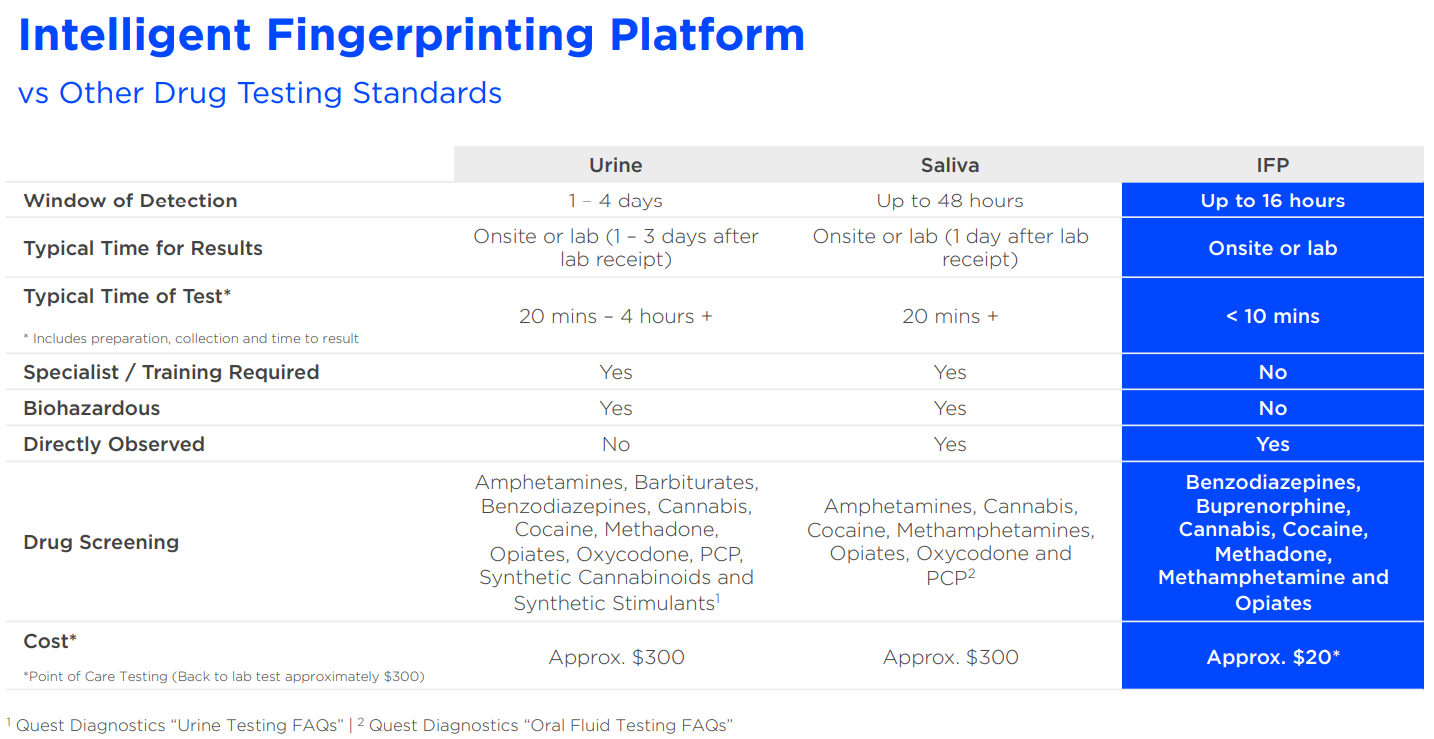

Comparison to Conventional Drug Testing MethodsThe Intelligent Fingerprinting (IFP) Drug Screening System is disrupting portable drug testing through fingerprint sweat analysis and has the potential for broader applications in additional markets (i.e. fertility tests and ketones). The system is very accurate, and compared to urine and saliva testing, it is hygienic and not biohazardous as IFP testing requires no handling of bodily fluids. This eliminates specialist handling, collection areas, and clinical waste disposal.On top of that, it is a cost effective method for screening for recent use of drugs including opiates, cocaine, methamphetamine, and cannabis; accurate lab tests of urine and and saliva cost an incremental ~$300 each, while IFP costs around $20 per test. The test time also takes less than 10 minutes compared to urine and saliva tests which take days to return results and oftentimes take considerably inconvenient to conduct, especially if the tests are not conducted right at the workplace. The lower cost and rapid results allow for a combination of increased workplace testing and reduced costs.IFP also has a window of detection of up to 16 hours, as opposed to traditional methods which detect drug use up to 4 days prior. The detection window and the rapid turnaround makes it useful for “fit-for-duty” impairment drug testing where results can be obtained quickly enough to obtain a negative drug test and not disrupt workflows in safety-critical industries. Due to these superior attributes, the IFP platform has a large number of positive case studies published and it appears customers are very happy with the program, its ease of use, promotion of drug screening and subsequent disincentivizing of employee drug use, as well as drug screening cost savings.

Regulatory and Commercial ProgressThe IFP device received a CE Mark and is commercialized in the UK and Australia, with over 360 customers, and INBS is eyeing an expansion into mainland Europe where they recently had a patent granted in 17 different European countries. The company received FDA guidance in June 2023 in which the FDA provisionally stated that the IFP system would fall under a Class II Type Opiate Test System, which would fall under a 510(k) pathway, requiring a pre-market notification to the FDA 90 days prior to marketing, which must include a comparison of the device to another marketed device. As such, Intelligent Bio Solutions must conduct a clinical trial to properly compare IFP to another type of test (a saliva test in this case), and determine according to FDA documentation that IFP:

has the same intended use as the predicate; and has different technological characteristics and does not raise different questions of safety and effectiveness; and the information submitted to FDA demonstrates that the device is as safe and effective as the legally marketed device.

As such, for now, the company’s strategy is to grow revenue in non-U.S. jurisdictions, such as the United Kingdom and Australia to bolster their financial position while pursuing FDA approval and proportionately reduce the loss. The company plans to commence a clinical trial in April to test the IFP system vs. marketed tests. An application for FDA approval is expected to be submitted in the second half of 2024 with potential approval by Q1 2025, which will open up a very large market for the company. So as of now, the company cannot pursue the U.S. market but they are ISO13845 certified, and FDA approval could serve as a large catalyst for INBS shares.The company also recently received NATA accreditation in Australia. This is a significant hurdle they have quickly jumped over that will improve their credibility in Australia as they ramp up their sales on that continent, a process that only recently was started.

The Biosensor

Intelligent Bio Solutions is not a one-product company. Their legacy asset, the biosensor platform, has the potential to test for up to 130 indications, ranging from glucose to immunological conditions and communicable diseases. Glucose monitoring was the primary focus for the company and they successfully developed a transistor-based biosensor that outputs a current based on the glucose concentration of saliva. Unfortunately, the correlation of saliva glucose measurement using the organic thin film transistor (OTFT) to blood glucose measurements was not as good as the company hoped for and the company they licensed from went bankrupt, so the Biosensor’s development is on pause and the company turned to focus on fingerprinting. That being said, the biosensor will likely move forward when the company is in a position to further fund its development; this is another technology with the capability to rapidly and inexpensively test a wide variety of indications.

Competition

Labcorp (NYSE: LH) offers urine tests with mass spectrometry confirmation for point of care and at patient services centers. Results are available within four hours. They also offer saliva tests which are available within days.Quest Diagnostics (NYSE: DGX) also provides similar services. The company’s saliva tests return negative results reported on the same day. The same goes for Thermo Fisher. Abbott Laboratories (NYSE: ABT) offers urine tests as well as synthetic marijuana saliva tests. OraSure (Nasdaq: OSUR) also has saliva-based tests but these have to be sent out to a lab to get results.Private competitors include Advin Biotech, which produced innovative urine and saliva tests, and LifeSign, which produced a rapid turnaround urine test.

Management

Intelligent Bio Solutions has experienced management. For instance, Spiro Sakiris, CFO, has a background in accounting, taxes and auditing which has proven. Harry Simeonidis, the company’s CEO, has a background in healthcare, medtech, and logistics, which is fitting for the company’s current focus. He was CEO of GE Healthcare ANZ for 10 years and led GE’s surgery business in Asia for 3-4 years. He is a six sigma black belt who has always been about bringing new products to market. He left GE and joined Intelligent Bio Solutions to make a difference, particularly in affordable, point-of-care, noninvasive technology. Management, while not owning a significant portion of the company right now, have all invested considerable sums of money into the company in the past and their payouts are contingent on successfully hitting milestones. Thus they have put skin in the game and are motivated to see the company succeed.

Financials

Aside from robust revenue and revenue growth, the company’s financials were its weakest aspect. As previously mentioned, the company recently raised $1.77 million from the exercise of warrants and for the issue of new warrants above market price. Subsequent to the warrant conversion, the company also raised $10.1 million in a private placement, priced at the market ($4.55/share) with tho sets of warrants (H-1 and H-2, each exerciseable at the same at-the-market price). This raise caused significant dilution but sets the company up for operational success and organic gross profit growth.The company had $1.12 million in cash as of Dec. 31, 2023, with current assets, (accounts receivable, R&D tax incentive receivable, inventories etc) of $2.94 million. With a second fiscal quarter net loss of $1.98 million driven by SG&A of $1.71 million, the company is still burning through significant amounts of cash and was inevitably going to find sources for funding such as the newly placed warrants above market price, and and the recent private placement. Now they likely have enough money to reach cash flow breakeven.Cash flow breakeven is estimated at ~$12 million in annual revenue. As the company produced robust growth with $0.199 million in gross profit, and gross margins are expected to eventually increase to about 50% or greater based on manufacturing and logistics, breakeven is targeted around the end of 2024 or early 2025. These projections do not include pro forma for FDA approval or any sales in the U.S. which would serve as additional upside. The recent $1.77 million from warrant exercise and the recent $10.1 million equity raise should provide more than enough funds for the company to reach cash flow breakeven early next year, and it’s possible Intelligent Bio Solutions will not need to raise money again. Notably, the H-1 and H-2 warrants are likely to bring in additional funds to the company. The H-1 warrants are exercisable within 18 months and the H-2 warrants are exercisable in 5 years, but that window is reduced to 20 days if the company gets FDA approval.

Valuation

As of February 7, 2024, there were 2,147,789 INBS shares outstanding, with the majority of warrants (606,064 warrants at $4.50) existing based on the warrant replacement from the $1.77 million warrant exercise deal, for a fully diluted share count total of about 2.75 million shares. Following the recent private placement, estimated shares outstanding increased to 4.37 million with a fully diluted share count estimated at 9.42 million shares outstanding. While the large increase in fully diluted shares is obviously negative, the proverbial Band-Aid has been ripped off and the company may finally see smooth sailing in their growth and cash flows.We believe the company’s shares are significantly undervalued based on revenue multiples and long-term earnings potential, with the company being close to cash flow breakeven with a target of the end of 2024 or early 2025. The company announced unaudited Q3 and nine month revenue results which showed quarterly sequential revenue growth from robust growth in Q2 to $0.82 million in Q3 (80% growth from last year’s Q3).INBS has a PSG (price per sales growth) ratio of 0.027 given a current estimate of $3.28 million in annualized revenue (the vast majority is UK-based business), where 0.0-0.2 is considered attractive (lower is better) and have been found to outperform the overall market. While >100% revenue growth cannot be expected for long-term growth, the company may be able to support triple-digit growth for the short term (next few years), considering they are targeting Asia, Europe, and the U.S., where the TAMs are approximately $2 billion, $2.5 billion, and $4.5 billion respectively—much larger markets than just the UK, where almost all of their current revenue is derived from. In Australia where they recently launched sales, and Asia, they’re targeting a distributor model (with required revenue growth and upfront payments which could reduce the company’s requirement for cash) which should keep a lid on their overhead expenses while allowing them to access these large markets immediately. As for direct sales, the conversion rate in the UK after a demonstration has been given is in the high 80% range so the cost of a sales force is money well spent. NATA accreditation should improve their ability to sell in the ANZ geography. These markets, UK and ANZ, could grow to $50 million and $25 million annually for INBS.Currently, the typical customer is a small-to-medium-sized company with 200-1000 employees, with an initial order of $50-100k in the UK ($40k in Australia), including readers (~$1500) and cartridges (~$20). The repeat business, cartridges, is typically $50,000 in annual recurring revenue with the company’s current cartridge business bringing in up to $50,000 monthly, which should grow fairly quickly in the next few years as they add more customers. The company also intends on creating next-generation readers to upsell to existing customers in the future, and with increased brand recognition and certifications, they can go after very large companies with much larger contracts. Once FDA approved, the company has the opportunity to develop the next-generation reader to include new features, such as connectivity and remote software/cloud-based processing, so that the software working in the background can be monetized and collect data. With over 500,000 tests, if the company could collect data, they could find the overall prevalence of certain drugs (while maintaining personal anonymity), and sell that information to institutions and governments.Intelligent Bio Solutions’ gross margins should improve with scale compared with their current margins, as the company reaches higher manufacturing capacities. Manufacturing at optimal capacities is expected to yield 60% gross margins and the company will optimize costs by managing capacities utilizing either in-house or contract manufacturing. In the United States, which covers a larger geographical area, transportation plays a large role in the costs compared with cartridge manufacturing, so localized manufacturing may be a better option.INBS’ revenue is currently approximately doubling year over year, and the company is reducing costs where it makes sense to do so, so it is arguable that the company, in its sales infancy, should be valued at 10x sales, or about $32.8 million ($8.20/share based on 4.37 million shares). Fully diluted shares are not counted in this calculation as the proceeds from warrant exercise could bring the company over $20 million in cash which is antidilutive given the magnitude of cash potentially received (and exercised at a price well above current market price).Over the long term, it’s conceivable the company could reach hundreds of millions in revenue globally. With gross margins at scale expected at >50% and net margins expected between 10-20%, the company could then easily fetch a P/S ratio of around 2.0 on European, United States, and Asian and ANZ sales of $200 million. This would value the company at $400 million. Using a higher fully diluted share count estimate of 9.42 million, the shares would be valued $42.55. There is significant upside potential for INBS shares given the company continues to grow while minimizing or preventing further shareholder dilution.

Catalysts

Intelligent Bio Solutions has several upcoming catalysts this year aside from earnings reports which have been well received recently as the company has shown investors its ability to post robust revenue growth and improved cash burn on the way to profitability.

The company is anticipating FDA approval for the IFP system in Q1 2025, which will open up the largest drug screening market in the world to them, where the company’s revenue opportunity is in the hundreds of millions with drug screening volumes being much higher. Distribution agreements signed or product launches in Asian markets could also serve as catalysts, though investors will likely be focused on topline revenue, gross margins, and for now, cash burn.Accretive acquisitions, depending on deal structures, could be catalysts for the stock. Sometimes investors see acquisitions as an expense when a company is not cash flow positive; however, the Intelligent Fingerprinting acquisition Intelligent Bio Solutions made has allowed them to progress rapidly into a commercial organization. These acquisitions would have to be in line-of-vision for the company and have some sort of operational synergy for both parties, with criteria including healthcare screening and software, noninvasive technologies, a revenue model that grows (such as IFP’s razor-razorblade or a subscription model), and affordability. Management is not as interested in one-and-done products, focusing on models that offer repeat business, and they are not interested in paying lots of upfront cash.With the company’s increasing momentum, it’s possible that they could start signing large, global organizations. Sales contracts with large companies could have a very significant impact on the company’s revenues and announcements of such contracts could each serve as catalysts for INBS shares.

Risks

INBS shares are still somewhat at risk of dilution since the company is not yet profitable, although profitability in the near term is reasonably likely. Other than financing risks, the company’s main risk is its requirement for a clinical trial and FDA submission. However, the company does not need FDA approval to reach profitability. For such a small company, the risks are not very numerous and the gravity of the risks, aside from the possibility of dilution, is fairly low. Dilution risks for stocks like INBS, especially those in drug development or launching drugs or medtech devices, are typically high; however, the market has received Intelligent Bio Solutions’ earnings reports well and the company has raised money above or at market prices, so the risk of further massive dilution from poor shareholder support is relatively low.

Conclusion

Distributor deals and earnings reports, along with market sentiment, will determine INBS shares’ near-term future as Intelligent Bio Solutions navigates its way to profitability, which is in line of sight. The Intelligent Fingerprinting system works very well and is set to disrupt the marketplace. Sales have been successful so far with the market reacting very well to earnings reports. The main risk with the company, their financing gap, has been addressed, so further positive market reactions to their robust sales growth is likely. The company has been derisked in the medium term as it has been recapitalized and its revenues are growing.The company is headed in the right direction and likely has a bright future ahead as a successful commercial entity that may soon be able to support additional product development like its Biosensor. With additional IFP and Biosensor testing markets (aside from illicit drug use detection and glucose monitoring), as well as management’s desire to make accretive, synergistic acquisitions, shares could be multi-baggers from these levels as the company disrupts the healthcare testing, monitoring, and diagnostics market with its intelligent, rapid, accurate, and affordable solutions. INBS is shaping up to be a multi-bagger, but with all small companies, investors should carefully and appropriately weigh investment positions to account for risks.More By This Author:MAIA Biotechnology: Undervalued With Eye-Popping Cancer Data And Partnership Potential