The US dollar is extending its advance as the divergence theme moves into overdrive. The dollar has drawn close to JPY119.50. The euro has fallen to new lows near $1.2320, having been turned back from $1.25 on Monday. The Australian dollar has been pushed briefly below $0.8390.

The main exception is sterling, which is holding its own after a stronger than expected service PMI. Although it slipped below yesterday’s low, Monday’s low near $1.5585 remains intact, and sterling is trading around 3/4 a cent above there near midday in London.

The divergence theme has been underscored by the comments by Fischer and Dudley reaffirming the signal by Fed leadership that mid-2015 rate hike is still “reasonable”. The disinflationary impulse from the drop in energy prices is temporary. Instead, they emphasized the growth implications.

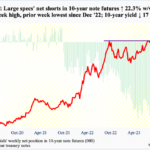

There has been a backing up of US interest rates too. The 2-year yield is near 55 bp, which is the upper end of the range seen in recent weeks, and represents a 10 bp increase since Monday’s lows. There is increased speculation that the “considerable period” phrase in the Fed’s statement is likely to be diluted or dropped as early as this month. Meanwhile, the 10-year yield is near 2.30%, which is a 15 bp increase since Monday’s lows.

In Europe, the service PMI was slightly disappointing at 51.1 from 51.3 of the flash and 52.3 in October. Germany was unchanged from the flash (52.1) but France’s downward revision wipes out the improvement that the flash suggested. France’s service PMI slipped to 47.9 from 48.8 of the flash and 48.3 in October.

The pleasant surprise came from Italy. The November service PMI rose to 51.8 from 50.8. The consensus was for 50.2. It was Spain that disappointed. The service PMI fell to 52.7 from 55.9. The market had expected a smaller decline to 55.2.

In addition, the euro area October retail sales in October rose 0.4%, slightly less than expected, and managed to retrace only a small part of the 1.2% decline in September (was initially -1.3%). This week’s data provides a poor backdrop for tomorrow’s ECB meeting. Everyone agrees that the ECB staff is going to cut its forecasts again and the Draghi will be dovish. This goes practically without saying. The key issue is whether the ECB expands the assets it is purchasing (to include supra-nationals, like EU, EIB, EFSF, ESM bonds like we think are “low hanging fruit), or does it announce its intentions to buy sovereign bonds, as some expected.