Many income investors, especially those focused on the best high dividend stocks, often rely on slow but steadily growing companies to make up the core of their diversified dividend portfolios.

And among such companies, certain dividend kings, stocks with 50+ consecutive years of payout growth, represent some of the best time-tested, low risk names you can find on Wall Street.

Let’s take a look at Genuine Parts Company (GPC), a business that’s seen sales and profit growth in 84 and 73 of the past 89 years, respectively, and which has rewarded dividend lovers with an impressive 61 straight years of dividend increases.

Despite the company’s attractive long-term history, Genuine Parts Company’s stock trades at an 18-month low, driven by disappointing auto industry trends and fears over Amazon’s (AMZN) entry into the automotive aftermarket parts industry.

Let’s take a closer look at this dividend king to learn more about the potential headwinds it faces and whether or not the stock’s current weakness could be an opportunity for long-term dividend growth investors.

Business Overview

Founded in 1928 in Atlanta, Georgia, Genuine Parts Company is one of the largest (#1 or #2 market share in all segments) replacement part makers in the automotive, industrial, office equipment, and electronics industries.

The company markets its products in the US, Canada, Australia, New Zealand, and Puerto Rico through a large network including 103 North American auto and industrial distribution centers, and 6,700 NAPA auto parts stores.

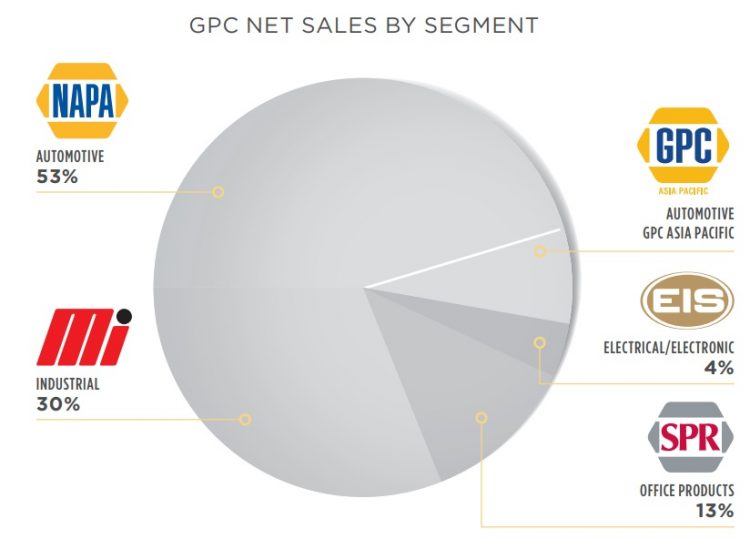

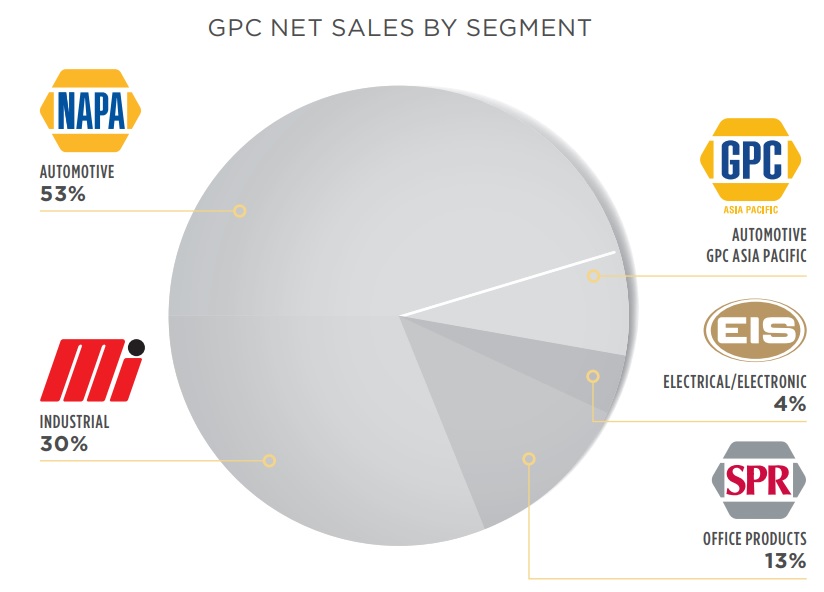

GPC’s sales are derived from a diverse group of well-known industry brands including NAPA auto parts, Motion Industries (industrial components), EIS (electrical components), and SP Richards & Company (office products).

By far the most important business segments are the automotive and industrial units, which combined made up 83% of 2016 sales.

Source: GPC Annual Report

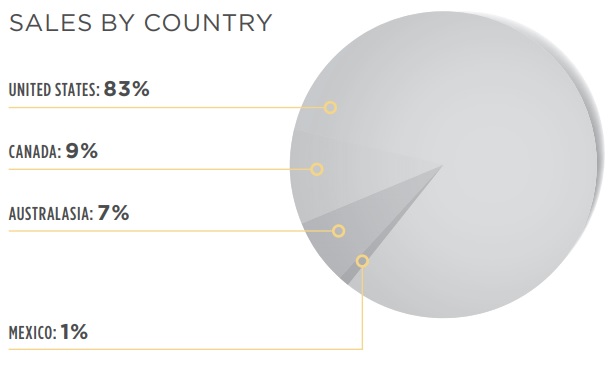

Similarly, North America represents the company’s dominant market, generating 92% of last year’s revenue.

Business Analysis

The key to over half a century of steady dividend growth is a business model that is protected by some sort of moat, meaning some kind of competitive advantage that allows a company to maintain pricing power while growing its market share.

In the case of Genuine Parts Company, its moat is courtesy of two main factors: the company’s massive distribution network and its trusted brand names.

For example, NAPA auto parts has a total of about 8,300 global stores, serving over 17,000 global service centers.

Meanwhile, Motion Industries has a 70-year history of providing quality products to industrial firms like Halliburton (HAL), 3M (MMM), and General Electric (GE).

In fact, Motion Industries is closely tied into the entire global industrial base, with its components finding their way into roughly 6.9 million products around the world each year.

The second factor in GPC’s moat is its supply chain and large scale inventory ($3.2 billion at the end of 2016). This is because NAPA auto parts works in an industry in which inventory management and just-in-time delivery is paramount.

For example, an auto parts store generally doesn’t want to hold a lot of excess inventory because that represents a substantial capital investment. Similarly, auto repair shops generally will order components as needed, in order to service customers that just showed up in a timely manner.

GPC’s large network of distribution centers make it possible for its customers to order parts at a moment’s notice and have them generally delivered the same day, maximizing their inventory turnover, and thus sales and profits.

As one of the largest players, GPC can afford to hold more inventories and offer better delivery times than many of its competitors.

In addition, the auto parts and industrial component sectors are generally price inelastic, meaning that customers care far more about the reliability of products and the convenience of deliveries than they do about getting the absolute lowest price.

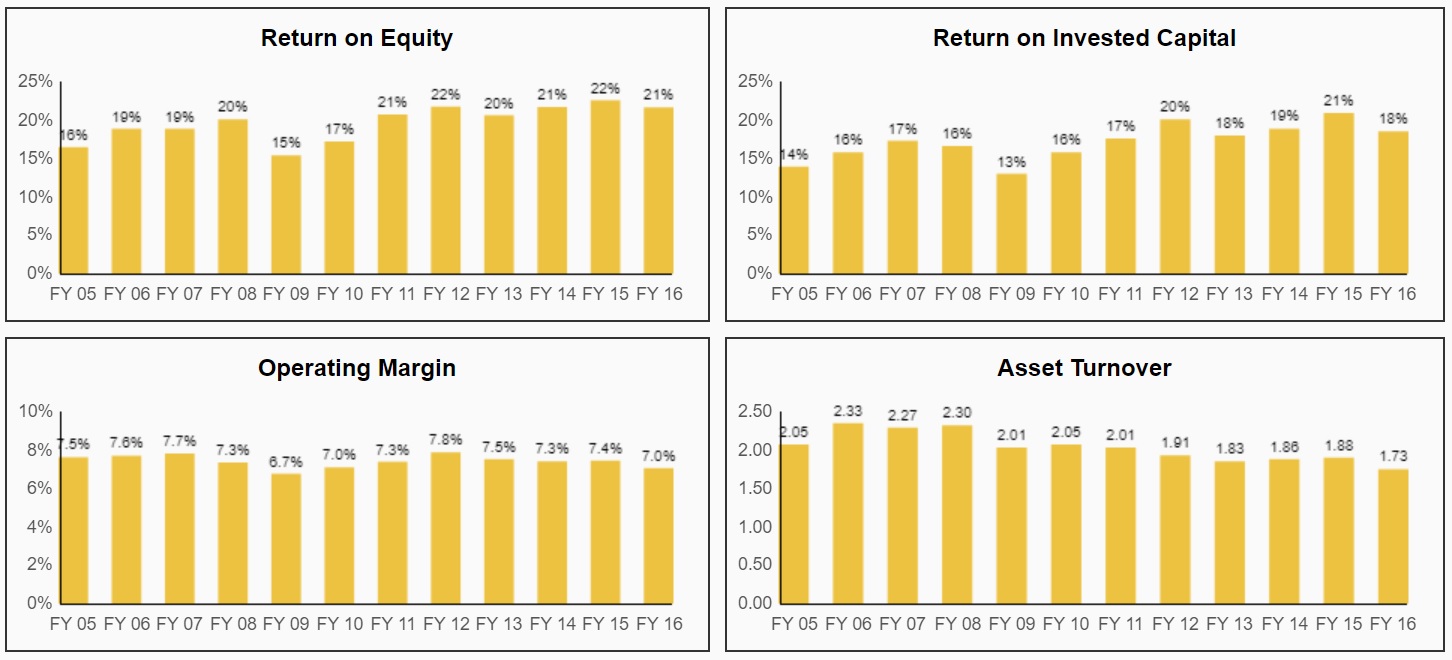

This allows GPC to maintain above average pricing power for its most important product segments, resulting in steady and even improving (thanks to growing economies of scale) margins and returns on shareholder capital over time.

Source: Simply Safe Dividends

Meanwhile, the company’s steady growth, another essential component to its dividend growth thesis, is courtesy of several factors.

First, unlike selling to original equipment manufacturers, aftermarket business is relatively stable. Vehicles and equipment breaks down and must be replaced. Therefore, the business is less discretionary.

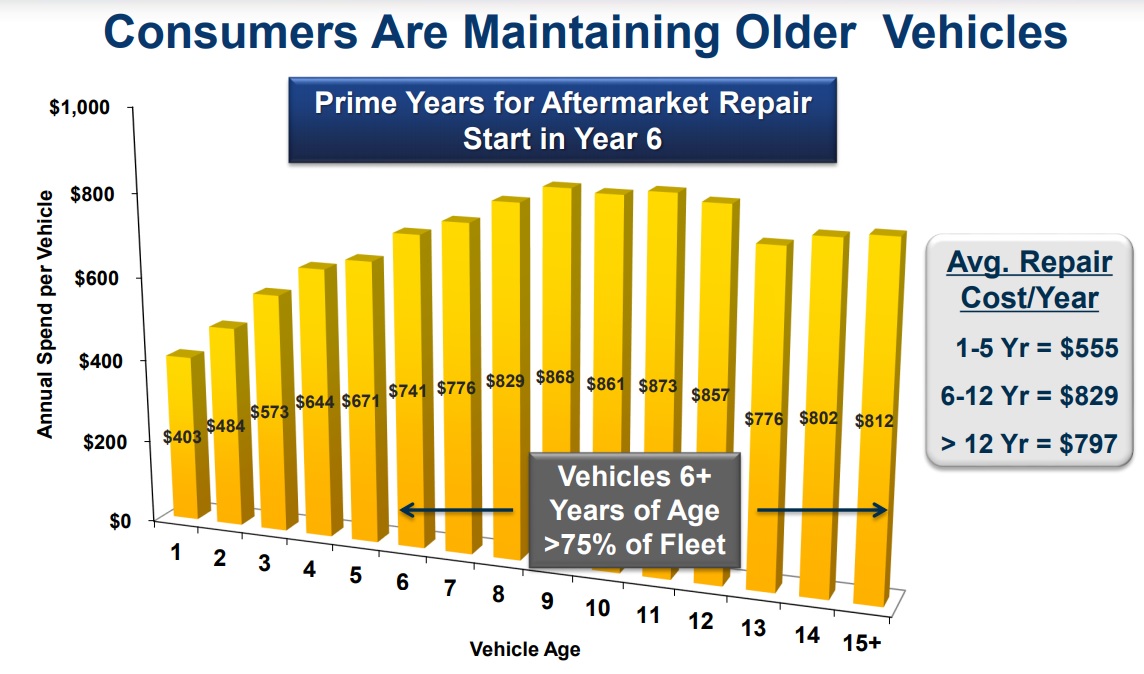

Additionally, the automotive aftermarket has been benefitting from the steadily improving reliability of vehicles over the decades, which allows consumers to own cars for longer, but only if they are properly maintained and repaired.

Source: GPC investor presentation