The week truly begins for the US Dollar today, which was trading flat on the day at the time this article was written, even though the Federal Reserve is not expected to move on rates. After all, the July FOMC meeting is an ‘off-cycle’ meeting, or one that won’t produce a new summary of economic projections (SEPs) and a press conference with Fed Chair Janet Yellen.

Accordingly, the policy statement will garner all of the attention. Given the steadfast support for a majority of Fed policymakers – particularly 2017 voting members – to raise rates again before the end of the year, it is possible that the Fed uses this ‘off-cycle’ meeting to further prime the market for the implementation of their balance sheet normalization strategy, which was outlined at the June meeting in the “Policy Normalization Principles and Plans” augmentation.

The Fed intends to wind down its balance sheet with an initial reinvestment cap for US Treasuries at“$6 billion per month initially, and will increase in steps of $6 billion at three-month intervals over 12-months, until it reaches $30 billion per month. For payments of principal that the Federal Reserve receives from its holdings of agency debt and mortgage-backed securities, the Committee anticipates that the cap will be $4 billion per month initially and will increase in steps of $4 billion at three-month intervals over 12 months until it reaches $20 billion per month.”

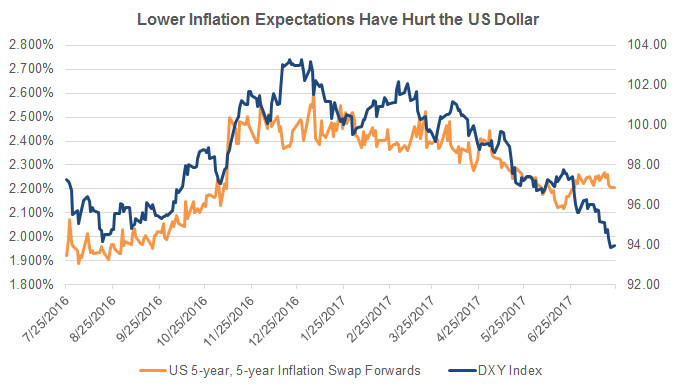

Chart 1: DXY Index versus US 5-year, 5-year Inflation Swap Forwards (July 2016 to July 2017)

The headstrong behavior by the Fed to plow ahead and continue with its desired tightening schedule could reawaken rate timing speculation, which has been decidedly dovish after recent weeks of poor economic data. The US Citi Economic Surprise Index closed last week at -52.6, down from -4.8 three-months prior. During this time, inflation expectations have dropped in parallel, with the 5-year, 5-year inflation swap forwards moving from 2.404% on April 28 to 2.207% on July 21. If the FOMC policy statement turns an eye to recently disappointing inflation readings, it may come across as a dovish blush to market participants.